Now that you have an LOI and transaction close date just around the corner (if you don’t, just pretend with me for now), you can expect a few expenses to come out of those millions that you are selling your company for. Besides the sale bonuses you are giving your team and potential equity you are investing in the new company, here are the most common seller fees you will encounter as part of an M&A transaction:

- Advisor Fees (Investment Banker, M&A Advisor, or Business Broker)

- Attorney Fees

- CPA Fees

Other expected fees:

- Indemnification Escrow

- Tail Insurance

While there will likely be other amounts subtracted from the closing amounts, such as network capital shortfalls, deferred revenue amounts, and other non-current liabilities, we will just focus on the fees listed above for now.

Advisor and other Professional Fees

I’ve written a number of blogs on the various M&A fees you will encounter in a transaction. But I wanted to update you with the latest fee schedule according to a recent 2023-2024 M&A Fee Study done by Firmex.

Advisor Success Fee

Most M&A advisors work for a success fee. A success fee can either be a fixed specified number or calculated as a percentage, depending on deal size. The study asked advisors across multiple industries what their success fees are for different deal sizes, and summarized as follows:

• $5M deals: 4.7% – 8% (with a 6.3% average)

• $20M deals: 2.3% – 5% (with a 3.8% average)

• $100M deal: 1% – 2.8% (with a 2.1% average)

The success fee is payable at closing either as part of the funds distribution or as a separate wire directly from the seller. There are various parts to advisor fees (with an increasing emphasis on engagement fees), so be sure to read my entire post to learn more.

Attorney Fees

Also under advisor fees are your M&A transaction attorney fees. Attorney fees paid by the seller are always less than what the buyer pays, as the buyer is responsible for drafting the contracts and the seller’s attorney just modifies as needed and provides the appropriate schedules. Don’t get me wrong, there is a lot of time the seller’s counselor will invest in a transaction, especially if an F-reorganization is involved, but the fees will be less than what the buyer pays. You can expect these fees to range from as little as $25K up to $65K, depending on the number of separate agreements and whether an F-reorg is part of the transaction. Look into options like hourly vs a fixed fee when investigating fees for an M&A attorney. I have seen some fixed fee arrangements work out nicely.

CPA Fees

Finally, under advisor fees, you will want to include your CPA, who will let you know what the tax ramifications will be of the transaction. Whether you have an S-Corp or C-Corp, there are certainly things you can do to minimize your tax obligation, and a good CPA will advise on best practices. I see pre-sale tax planning run anywhere from $3K – $10k, depending on the complexity and whether multiple partners and states are involved. If you need them to assist with forecasts or accrual-based accounting, it can go up from there.

Non-Advisory Transaction Expenses

Finally, there are a few non-advisory transaction expenses, such as escrows and insurance, or more specifically, “tail” insurance.

Tail Insurance

Tail insurance is insurance that the buyer will want you to get to cover the company post-transaction for anything that might have happened “pre” transaction, but that was not disclosed or acted upon until after the sale of the company. This usually includes one or more of the following types of insurance: E&O, D&O, Cybersecurity, EPL, and Commercial, just to name a few. These tail insurance policies are usually for 3 – 6 years after the sale and can run between $15K – $40K, depending on company revenue.

Besides what the buyer requires you to purchase for tail insurance, you may also want to buy some for your own peace of mind; most commonly, I see EPL (Employment Practices Liability) and Cyber Security. These tail insurance policies are usually purchased just for a couple of years, as you won’t be required by the buyer to keep them longer and usually, after a couple of years, the likelihood of a claim goes down dramatically.

Indemnification Escrows or Hold-Backs

Finally, we have indemnification escrows or hold-backs, which are typically 10% of the purchase price, sometimes less. These are funds that are held in escrow by the buyer for a period of 12 – 18 months and are returned to the seller if no material deficiencies are found.

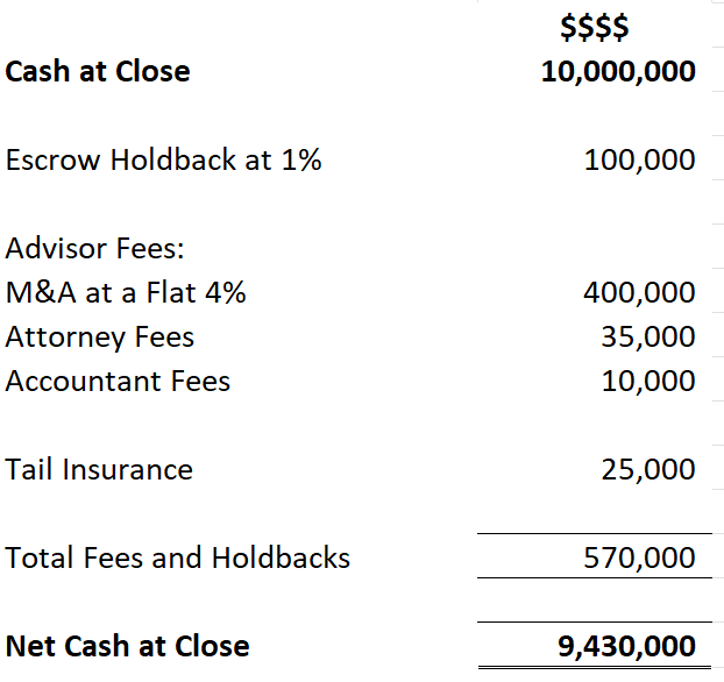

Example

Let’s put this to life using an example. Let’s assume you receive $10M cash at close. Here is how this might look:

In addition to these fees, you might have a net working capital shortfall or other special indemnification for something like sales tax in states where you might be deficient. Or you might be taking some of your proceeds and investing it in the new company, which then also reduces your cash at close. Of course, in the end, it is also taxed, but let’s not complicate our example.

My point in this post is to give you a realistic example of the types of expenses you can expect from those millions you just sold your company for, and to help you be aware of them when you are doing your own cash planning.

What Made This Latest Deal So Successful

What Made This Latest Deal So Successful