You signed the LOI. You think you have a deal. And then the questions start.

Requests for more data. Follow-ups that don’t quite make sense. Numbers you thought were solid suddenly being challenged. Before you know it, the tone changes and the deal you thought was done starts slipping.

It’s something most founders don’t see coming. The LOI feels like the finish line, but it’s actually where the real risk begins.

I was reading a recent report from Axial analyzing failed transactions in 2025, and it confirmed something I’ve seen play out in real deals over and over again. They looked at 75 deals that fell apart after an LOI had already been signed.

What they found is simple and, frankly, a little uncomfortable: deals don’t fail because of price. They fail because the business doesn’t hold up under scrutiny.

In my own experience, I’ve only had two deals break after LOI. Both times, it came down to the same issue: the data didn’t hold. Either it couldn’t be delivered on a timely basis or the numbers kept moving during diligence. Once that happens, the deal is already in trouble.

What the Axial data shows is that this isn’t an outlier; it’s the pattern. The number one reason deals broke wasn’t financing or market conditions. It was diligence.

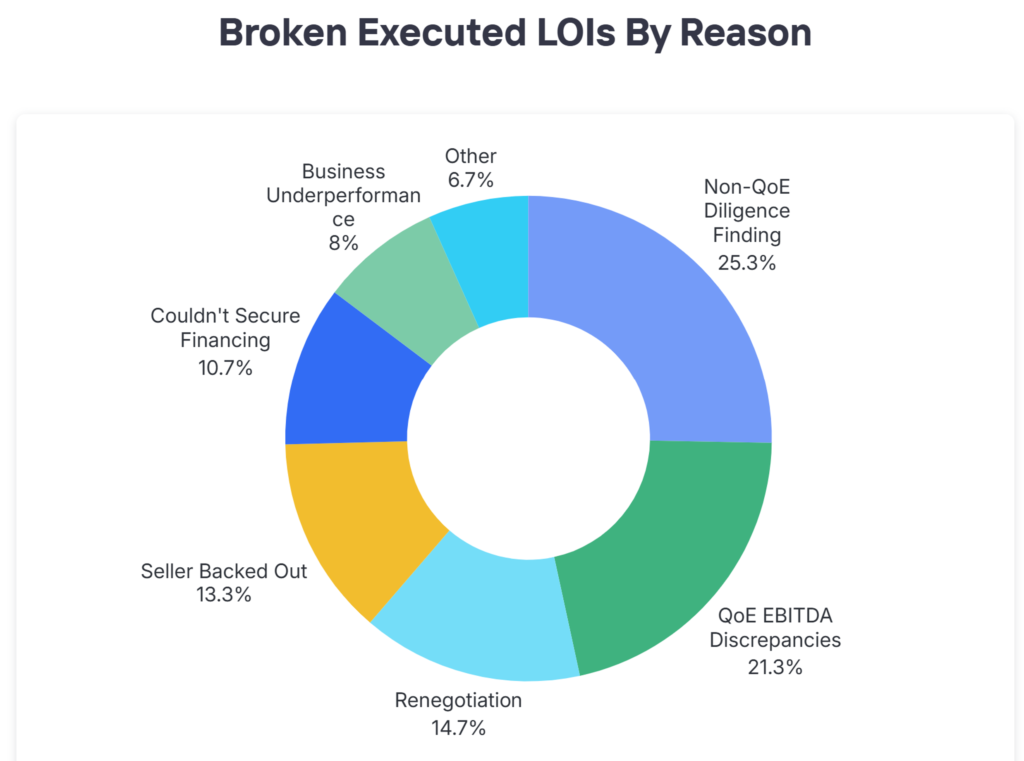

Top Reasons Signed M&A LOIs Are Broken

Here’s how those broken deals actually break down:

Non-QoE diligence findings alone accounted for over 25% of failed deals, and another 21% came from discrepancies in EBITDA uncovered during Quality of Earnings work. That means nearly half of all broken LOIs come down to the same issue: what was presented is not what actually exists. And notice that financing issues were not driving deal failure.

But this rarely shows up as one big, dramatic problem. More often, it’s a slow erosion of trust. The story doesn’t match the numbers. Addbacks don’t hold up. Revenue isn’t as recurring as it was positioned. Or risks that were always there finally become visible, whether that’s customer concentration, contract issues, or compliance exposure. These aren’t new problems. They’re just being seen clearly for the first time.

Then there’s the issue I see over and over again in the data and in conversations with founders. The financials move during the process. Numbers change. Reports don’t tie. Data takes too long to produce. Buyers don’t expect perfection, but they do expect consistency. Once that consistency is gone, confidence goes with it.

At that point, the deal usually shifts into renegotiation, or what we call a retrade. The buyer adjusts price or structure to reflect what they’re now seeing. About 15% of deals break right here because the two sides can’t come back together. From the seller’s perspective, it feels like the buyer is reneging. From the buyer’s perspective, they’re reacting to new information. Either way, the outcome is the same – the deal dies.

What’s changed over the last few years is important. Financing used to be the biggest risk in getting a deal done. Today, it’s not. Capital is available and buyers are active. But scrutiny is higher than it’s ever been. The shift is clear in the data. Financing issues now account for only about 10% of broken deals, while diligence-driven issues dominate.

How to Keep Your M&A Deal from Falling Apart After the LOI

So, what does this mean for you as a seller?

It means the deal is not won at the LOI. It’s won before it. If diligence is the first time your numbers are being pressure-tested, you’re already behind. If risks are first being uncovered after exclusivity starts, you’ve lost leverage. And if your financials can’t be delivered quickly, clearly, and consistently, the buyer will assume the worst.

I hear this all the time from founders. They get to an LOI thinking the hard part is over when, in reality, the hardest part hasn’t even started.

And I understand why. You’ve been running your business for years. The numbers make sense to you. The story feels right. But buyers aren’t looking at your business the same way. They’re testing it line by line, assumption by assumption, risk by risk. And if something doesn’t hold, they don’t ignore it. They reprice it, or they walk.

That’s why my deals rarely break. Not because nothing comes up in diligence (something always does), but because we do the work before the LOI. We normalize EBITDA before going to market. If the adjustments are significant or complex, we require a sell-side QoE in advance. We pressure test the numbers early and surface risks before the buyer ever sees them. By the time we get to an LOI, there are fewer surprises left to find, and the ones that do come up are expected, explained, and already framed.

The sellers who get to the finish line tend to do three things differently:

- They pressure test their financials before a buyer ever sees them.

- They normalize EBITDA the way a buyer will.

- And they surface risks early, before those risks get used against them.

It’s not complicated, but almost no one does it.

Preparation Before the LOI Protects Your Deal After the LOI

A signed LOI feels like a win, but it’s not. It’s the moment your business gets tested. If your financials are clean, consistent, and defensible, the deal moves forward. If they’re not, the deal slows, gets repriced, or dies completely. That’s the difference, and it’s almost always based on what you do before the LOI is ever signed.

If you’re thinking about selling in the next one to three years, this is exactly why I created my course, Getting Your Financials Ready for a Sale. Because if your financials don’t fully tie, your EBITDA adjustments aren’t clearly supported, or your numbers don’t hold up under scrutiny, buyers will find it, and they will use it. This course shows you how to fix that before you ever go to market, so you don’t just get an LOI, you get to the finish line with the value you expect.

The Next Wave of MSP Consolidation Is ERP – And It’s Already Underway

The Next Wave of MSP Consolidation Is ERP – And It’s Already Underway