It has been over two years since I have written about M&A fees, and I felt it was time for an update. After all, a lot has happened in two years! While COVID temporarily took its toll on many partners’ revenue, it has also catapulted several to their largest year-over-year growth in their company’s history.

While COVID did dampen deals and changed some of the terms, the industry certainly has come back with a vengeance. So, what does that mean for M&A fees? With so many buyers looking for sellers, is there a fee hike on the part of advisors and bankers due to all the activity?

This year, Axial and Firmex teamed up to provide the 2021-2022 M&A Fee Guide. Here are the highlights and takeaways from my personal experience over the last two years. Keep in mind, this survey was done across multiple industries with technology advisors representing less than 14% of the respondents.

The COVID-19 pandemic may have affected most areas of life and business, but it had little impact on the fee structure of middle market M&A advisors. According to the guide, only 8% of advisors (across all industries) say they have changed their fees in response to COVID-19. Of those, the most common adjustment was to lower or eliminate up-front fees.

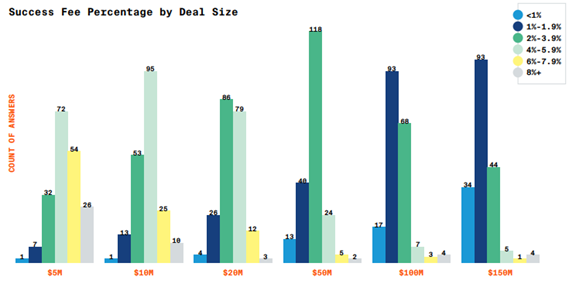

M&A Success Fees by Deal Size

While most of the advisors surveyed don’t formally use the Lehman formula*, their effective fees are lower for larger deals. The survey asked advisors about their success fees for various transaction sizes.

For deals valued at $5 million and $10 million, the most common fee is between 4% and 5.9%.

For $20 million and $50 million deals, fees are most likely between 2% and 3.9%.

And for deals of $100 million and $150 million, the most common fee range is 1% to 1.9%.

In every deal size, however, the average fee inched up compared to a year ago. For $10 million deals, the share of advisors charging below 4% fell to 34% from 48% last year.

So why are advisors charging more for smaller deals? Most advisors will tell you that small deals require just as much work as large deals. In fact, sometimes they require more work due the lack of experience or sophistication of either the buyer or seller, so there’s more hand holding on the part of the advisor. Ultimately, advisors are selling their time, so it makes sense that fee percentages come down as the transaction sizes increase.

The survey does say, however, that four out of five advisors haven’t seen any more pressure on fees in the most recent year than they did before. Of those that do feel fee pressure, only about one-third say they have cut their fees. Many say they are standing firm, explaining the value of their services. Indeed, in an open-ended question asking for comments on fee pressure, 3% of advisors volunteer that they have increased fees over the last year.

One last thought on fees is best summed up by my colleague Peter Lehrman, CEO/Founder, Axial:

“M&A advisors who are charging more than 5% are almost extinct, and they will likely die off completely over the next decade. The tools, data, and automation available to help M&A advisors deliver great outcomes for their clients are making it increasingly impossible to charge those 20th-century prices.”

I couldn’t agree more.

Work Fee or Commitment Fee

In addition to a success fee, most advisors charge a work or commitment fee. A work fee, commitment fee or engagement fee is a one-time fee that advisors charge for their efforts to sell a company, which is payable whether or not a deal is consummated. Most advisors (42%) charge this fee, while 35% charge a monthly retainer. Monthly retainers vary as well, and can range from $2,500 – $5,500 easily for lower mid-market companies. For those who charge this one-time fee, the majority (55%) charge $15,000 or more. 36% percent charge between $5,000 and $15,000, which is typically what I see for companies under $50M in revenue.

Minimum Success Fee

A minimum success fee is standard in the middle market and lower middle market. According to the survey, they are used by two-thirds of all advisors, regardless of industry specialty. Minimum success fees also vary and are usually tied to the overall valuation of the company. It’s rare to see an agreement that doesn’t have one stated, as it sets the watermark value expectation between the advisor and client for what is acceptable. It’s rare to see a minimum success fee lower than $75,000 these days, which, if you calculate a 3% success fee on that, the seller needs a transaction larger than $2,500,000 to break even.

Conclusion and Some Final Thoughts

As I mentioned in my article two years ago, any broker who is willing to work only for a success fee should be viewed with caution. Their reward only comes when your company is sold, and since they are not being paid to find you multiple buyers or offers, they will stop at the first offer that looks like it might work. So, while you want to negotiate the lowest fee possible, don’t try to be penny wise and pound foolish here.

Selling your company is the most important financial decision you will probably ever make. The industry’s fee structure gives comfort to business owners that we are as committed to their deal getting done as they are. And if you chose the right advisor who presents you with the best buyers, you will find that payment of the fees at a deal’s closing is the easiest check a client ever has to write.

But know that, as advisors, the success-based fee structure also forces us to be discerning on the types of clients with whom we engage. We are forced to consider not just the strength of the company and its industry, but also the integrity of management, their commitment to selling, and their ability and willingness to ultimately get the deal done.

*The Lehman Formula (also known as the Lehman Fee or Lehman Scale) is a commonly used method for defining compensation owed to an investment bank or deal broker for arranging a transaction. In the 70s and 80s, it was commonly used for fundraising and private placement transactions. Today, it is much more common in lower middle market acquisitions.

The original formula applied to transactions above $1 million and followed a 5-4-3-2-1 tiered structure:

- 5% of the first $1 million

- 4% of the second $1 million

- 3% of the third $1 million

The Optimal Time to Sell Your Company

The Optimal Time to Sell Your Company