Its been a busy year to say the least. When COVID hit, I thought for a brief moment the chaos and pause in travel, conferences and business in general might provide some much-needed whitespace on my calendar, but no! Why? Because my clients are in the technology sector, and technology service providers are what is keeping Zoom, Team and GoToMeeting calls running on schedule. Sure, M&A volume has taken a hit, but not in the tech sector.

For the first half of 2020, just under 20% of all Private Equity (PE) transactions completed were actually in the technology sector and this represents over 30% of deal value. Of these transactions, most were “tuck-in’s” to larger portfolio companies or the acquisition of smaller companies. And while Covid is killing the travel and entertainment industries, competition for good tech firms remains fierce amongst buyers. So, no rest for me as an M&A advisor to technology service providers. Here is what I have seen emerge as transactions have closed over the last few months.

It is not about price; It is all about terms

Many sellers have asked me if deal values have dropped during COVID. Part of me expected that to happen given all this chaos, but that is not what I have seen so far. EBITDA multiples remain solid, but what has changed are deal terms. And not necessarily in a bad way. There is a definite shift from cash at close to a note term payable over 1 – 3 years, with a good interest rate. Sure, everyone likes a ton of cash at close, but if the interest rate is good, then allocating the gain over a few years is not a bad tax strategy. Earn-out periods have in some cases been extended to allow for a later start or to allow for the seller to earn more over time. Again, in most cases, this is all better than taking a hit on the sales price.

Realistic projections are welcomed, regardless of how flat

Savvy buyers do understand that there are verticals and industries that are struggling now but will eventually bounce back, while others may not. While you may have provided projections at the beginning of the transaction or pre-LOI that were very aggressive, revising them down to be more realistic with current customer buying habits is welcomed (unless of course, you are hitting it out of the ball park). Revising projections downward has not killed any of my transactions, but instead has been appreciated so buyers can truly assess future cash flow. No one wants a surprise or to be blind-sided if the year does not end up as originally projected.

A strong customer base, even if they are not buying now is still gold

Many of your long-time customers may be holding off on new projects and still in the cash conservation mode even if they did receive a PPP loan. Most sophisticated buyers view this just as a timing issue. They know maintenance renewals still need to be paid, monthly subscriptions will be paid, and projects started and put on hold, will come back. If the customer has a track record of spending money with your company over the years, sellers are okay with a temporary hold on requests for new products and services. And many buyers have extended the earnout period to allow for this.

There is safety in smaller transactions

As I mentioned in the start of this article, many strategic buyers and even private equity firms are now looking down market to make smaller tuck-in acquisitions. While they take the same amount of time and effort as a larger one to complete, there is less risk should something not work out. I have seen deals as small at $1.8M in revenue get completed in record time. All this is good news for VARs, MSPs and ISVs who remain under the $5M and even $3M threshold that most PE would not have considered in the past.

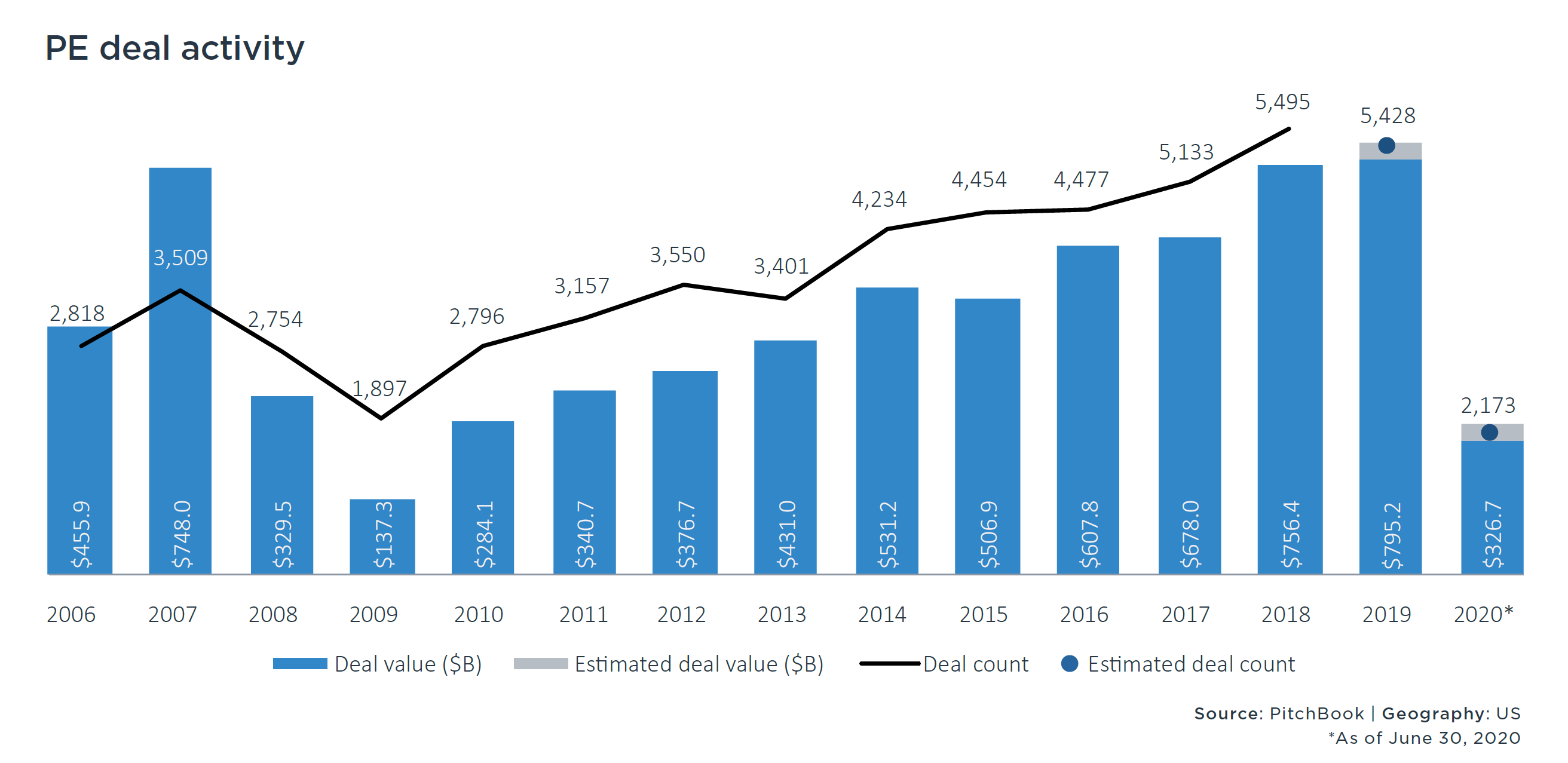

Private Equity still wants to invest their money

Over the last 5 years, private equity backed transactions represented roughly 50% of all completed deals in the US. In the second quarter of 2020, PE accounted for almost 62% of deals. A sharp decline in corporate-backed acquisitions paired with PE’s ability to react more nimbly to the pandemic are a few reasons behind this significant change. ¹

PE activity could also be driven by the record amounts of capital sitting on the sidelines ($1.7T as of July). All the while corporate revenue and earning growth will continue to be slow and lingering economic issues like high unemployment and consumer discomfort with public and social activities will keep many industries from bouncing back quickly.

So far, I have not seen one PE backed acquisition die during this COVID period. Even if I thought the deal was completely dead, it came back. I guess when you have money to spend, you spend. After all, a good company will always be a good company and PEG’s are willing to take that risk where the majority of strategic buyers will not in this current environment.

Final Thoughts

As we finish out 2020 and even into 2021, I believe we will continue to see a large number of deals continue to transact in the technology sector and it will continue to be private equity making the investment. What does that mean for strategic buyers? They will pay more. Once they return to the market.

And with less sellers at the table today, those that come to market will get more attention by those buyers looking for acquisitions. Who would have guessed all this in January? Here is to another busy 12 months.

Not sure if Private Equity is your best buyer? Be sure to take the quiz, Which Buyer Type is Right for you!

M&A Activity in Tech Sector is Resilient Despite Challenges of 2020

M&A Activity in Tech Sector is Resilient Despite Challenges of 2020