Catch up on any topics you might have missed from our newsletter series, Get Ready to Sell in 2025:

- Welcome: Get Ready to Sell in 2025

- The Steps Owners Should ACTUALLY Take to Get Ready for an Exit

- When is the Perfect Time of Year to Sell?

- Deal Timeline: What to Expect

- What is Your Company Worth?

- A More Specific Look at IT Valuations

- Why MSPs Sell for a Higher Multiple Than VARs

- EBITDA & Normalizations – The Hidden Money

- Recurring, Repeat and Renewals – Each Have Different Value

- The Number You REALLY Need to Sell Your Business For

- Best-in-Class Numbers – What %’s Should You Be Striving For?

- Common Seller Fees in an M&A Transaction

- Common M&A Agreements

- Normalization Adjustments Are NOT Just Personal Expenses

- From Planning to Profit: A Comprehensive Guide to Successful M&A Transactions

1. Welcome: Get Ready to Sell in 2025

Welcome to our newsletter series…

These curated emails will cover all sorts of topics specifically geared toward getting you prepared and in the best position possible to sell your company (whether you plan to sell this year or in 5 years).

The information in each newsletter is based on successfully completed transactions as a sell-side M&A advisor (and seller of 3 of my own companies), as well as lessons learned by other sellers.

Here are some of the exciting topics we will cover in depth in this series:

- When is the perfect time to go to market

- How long and what is the process involved in selling your company

- Valuations in the marketplace today

- Differences in valuations based on company type (MSP, VAR, etc.)

- A deep dive on recurring vs repeat vs contractual revenue

- Identify your EBITDA and normalizations

- Product margins you should be striving to hit

- Fees you can expect to pay in a transaction

- Documents you can expect to see in a transaction

- How to vet buyers and advisors

- Major mistakes to avoid

- And much more…

We also want to encourage you to respond to any of these emails with questions or requests for further clarification. We’ll prepare a special Q&A post to answer these questions as part of the series.

We think this is the most comprehensive, no-cost series you will find on how to begin an M&A transaction.

Even if selling is not in your plans for the next 3 – 5 years, there is a lot of information here to get you thinking about what an M&A transaction involves. You don’t want to miss it.

Remember, the most successful transactions are completed by those who plan and prepare in advance. And this series will help you get there!

Keep an eye on your inbox for your next newsletter (and add us to your email contacts so we don’t get lost in your spam folder)!

2. The Steps Owners Should ACTUALLY Take to Get Ready for an Exit

Welcome to our series, Get Ready to Sell in 2025!

Over the next several months, we will share important information to help you get ready for a possible transaction in 2025 and beyond. Even if you don’t plan to sell for multiple years, you will find the information in this series timeless. So, let’s get started!!

This first topic was inspired by an article written by MSP Success where they asked owners who plan on selling in the next 3 – 5 years what steps they were taking to get ready for a transaction.

Their top answers included items like cleaning up financials, attending an M&A session at an industry conference, talking with a broker, and more.

As an M&A advisor and former owner of three of my own companies that I sold throughout my career, I think the list is missing some really important items.

So I took the opportunity to discuss the The Steps Owners Should ACTUALLY Take to Get Ready for an Exit, as opposed to maybe the steps owners might THINK they need to take.

And for the steps that I do agree with, I offer a little extra guidance or resources that could help you accomplish them.

For example, the article discusses getting a valuation, and I recommend my Value Maximizer Assessment™, made specifically for IT companies, which will give you a very accurate picture of your potential market value and where you are leaving money on the table. It does require a code, so reply to this email with “VMA” and I’ll send you your access code.

And take a look at the article – I hope you find it informative.

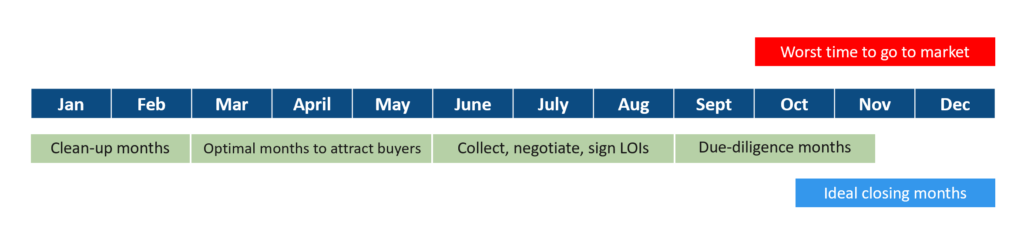

3. When is the Perfect Time of Year to Sell?

Welcome to our second topic of the Get Ready to Sell in 2025 series. Today is all about timing the sale of your company.

While deciding which year to sell is a very personal decision, our question today relates to when during the year is the best time to go to market.

And yes, there is a natural rhythm to M&A, just like there is to managing your own business either on a fiscal or calendar year. And really, it all relies on the rhythm of buyers.

So let’s start by discussing the worst time to go to market.

In the fall, almost every prolific buyer (I mean mostly PE firms and family offices, or strategic buyers backed by PE) is either:

a.) Beginning to wrap up a transaction

or

b.) In in the deep process of due diligence; whether that be financial, insurance, legal, or technology due diligence.

Everyone has the end of the year in their sights and knows that that is the ideal time to wrap up their transactions before the holidays hit.

Remember, it is not just the buyer involved in this process, but also:

- The accountants who are preparing the quality of earnings report

- The insurance team looking at your policies

- And the IT team looking at your infrastructure.

All of these outside consultants do not want to be working on projects over Thanksgiving or the holiday season (although we all know this can happen if a deal drags out or starts late in the year).

In this blog post, I explain in detail this timeline below:

What this shows it that, if you want the best chance for your company sale, you need to begin your go-to-market strategy in late February and March. These are the prime months active buyers seek new opportunities after wrapping up previous year deals in January.

Of course, not everyone can be ready exactly in March or April. But by July and August, most PE firms are at saturation levels; they don’t have the bandwidth to look intently at new opportunities because they already have a lot on their plate.

Remember, the goal here is to get as many eyeballs on your transaction as possible for multiple offers.

Make sure you read the entire post for the behind-the-scenes details on when the most ideal time is to enter into the market with your own transaction. In our next email, we will review the “deal timeline.”

See you back here soon.

4. Deal Timeline: What to Expect

In our last Get Ready to Sell newsletter, we discussed the perfect time of year to sell your company, as in which months are best to go to market.

This newsletter will focus more on how long a transaction takes from start to finish: a very common question asked by most business owners.

Assuming you don’t currently know who the prospective buyer is, a typical deal timeline is about 7 – 9 months from “going to market” to close.

Of course, there is extra time before you start looking for a buyer, and there is a stage post-sale where the companies integrate and the sellers work through any earn-outs that may extend this timeline.

If you already know the buyer (i.e., an unsolicited offer or you plan a transaction with a competitor), that timeline is actually reduced to about 4 – 5 months, since you don’t have to find the buyer and they are more likely to understand your business as a competitor or affiliate.

In a typical transaction, there are basically 6 stages in the M&A process:

- Preparation – This can take as little as one month or as long as three years to complete. This difference in time is usually due to how well your financials are done or whether they are in accordance with GAAP. Planning for 1-2 years is usually a good rule of thumb.

- Buyer Identification – When using an advisor, this usually takes a couple of months.

- Letter of Intent Selection – Hopefully during this process you have multiple LOI’s to choose from, and you will spend a few weeks just negotiating that final LOI.

- Due Diligence and Contract Negotiation – These two typically happen simultaneously, but the most prepared sellers (you will be one of those) have many of the due diligence items already in place in a virtual data room.

- Closing – I call this the last week of close. It is usually pretty hectic and requires a lot of numbers and last-minute accounting and reconciling. This stage also includes customer calls with your top 5 – 10 customers that the buyers will want to speak with.

And finally

- The Post-Sale Integration Process and Earn-Out – Again, this stage varies by the deal. If you receive a 100% cash offer, this step is almost entirely eliminated. But most deals have a 1- to 3-year earn-out that requires the seller to remain.

Owners need to be realistic about how ready they are for the process of selling their company, including the amount of time it takes.

I suggest sellers use the timeline above, along with the information in this article, to determine how long this process will be for them. I see many owners spend a year or two preparing before going to market. Personally, it took three years to get my last company ready for a sale.

Just be realistic when planning so you can have the best process possible when the time comes, rather than feeling overwhelmed or rushed.

5. What is Your Company Worth?

In most initial conversations I have with potential sellers, I get the big question:

“What is my company worth?”

Of course, with only minimal company information, that is a hard question to answer. But I do have some general responses that I can give pretty much every seller.

I’ll give an overview in this email, but you should take a look at my latest article to get more detailed information: What is My Company Worth?

A company’s value is determined by four major aspects:

1. Top Line Revenue and Growth – This is first and foremost. Of course, you cannot compare a $3M company with a $30M company for valuation purposes (the larger the company, the higher the general value). Revenue growth is important as well. Low or no growth, unless during Covid or a recession, is an indication of problems. Otherwise, a growth rate of 10% – 20% per year over the last three years is reasonable and expected by buyers. The higher the revenue, the higher the value. The higher the growth rate, the higher the value.

2. Gross Profit Margin (GPM) – Remember, if you are comparing two $5M companies that sell similar products, the one with the higher gross margin is more valuable. Gross margins vary by industry and within an industry; meaning you cannot compare the gross profit margins of an MSP (managed service provider) with an ISV (independent software vendor), for example. I would even say that GPM is more important than bottom line revenue, because general and administrative expenses are fluid and expendable. Of course, in order to properly state gross profit margins, you must accurately account for cost of goods sold, which most people don’t do correctly. Here is a great article that talks about margins and best-in-class percentages.

3. Recurring Revenue – The next most important aspect for valuation is the percentage of revenue that is recurring. The higher this number is, the more cash you will receive at close or the shorter the earnout period. In general, companies with over 50% recurring revenue see more offers than companies who have less. It has become a given and norm with all technology companies. But remember: repeat and recurring are two very different types of revenue. While repeat revenue does have value, it is not as highly regarded as recurring contractual revenue. Be sure to understand the difference, and be ready to show each type in your financials.

4. Industry Specialization and Intellectual Property – If you have some secret sauce that makes your products and services different than your competition, your multiples will increase dramatically. This is what truly skyrockets multiples. We all know the stories of companies that have no net income but astronomical multiples. The reality is: most people don’t have that strong of an industry specialization, so they try to distinguish themselves in other aspects, (i.e., people, location, experience).

There is also one aspect that can majorly reduce your value (even if you knock the four aspects above out of the park). Head over to my full article to learn what that aspect is.

I also provide an example scenario, and a generic visual that can help you begin to assess what your range of multiples might be.

If you are looking for a more detailed explanation on multiples in the technology services provider area, I highly suggest you check out my book, Get Acquired for Millions. In Part I – Driving From a Desire to a Deal, I go into great detail on multiples in our industry based upon organization type: VAR, CSP, MSP, ISV and developer.

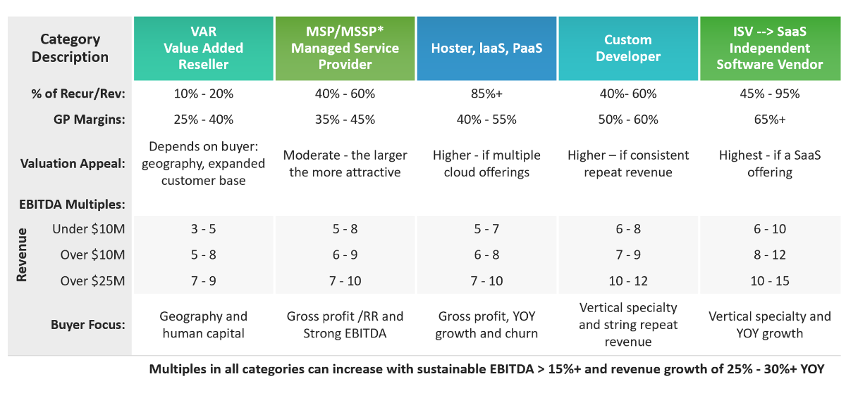

6. A More Specific Look at IT Valuations

In our last post, we took a general look at what your company is worth and talked about the four areas that help determine your value. In this post, I am going to get really specific about the multiples a company might expect based on partner type or organization focus.

In the chart below, you can see that I have divided the typical IT company into 5 separate buckets**. Each is different and unique in the type of services they offer to their customer base. While it is possible that your company has a combination of a few of these, you predominately focus in one area.

For example: You might sell and service an ERP, CRM, or Marketing Automation solution, and maybe you have even created some small add-on applications. So, you might say you are both a VAR and an ISV. The market, however, will look at you predominantly as a VAR. Therefore, that is the category you will be associated with, as that is where the bulk of your revenue is generated.

EBITDA Multiples Vary by Organization Type

You can see from the chart below that the EBITDA multiples vary greatly by the type of organization you identify with.

As you can see, MSPs under $10M in revenue range from 5x – 8x EBITDA, while ISVs can range from 6x – 10x with the same revenue. ISVs, especially those who have cloud offerings on a subscription basis, are usually garnering the highest multiples due the inherent high gross profit margins and high recurring revenue.

The chart also has the average recurring revenue rates and gross profit margins in each category. Compare yourself against these and see how you stack up. If you are greater than these averages, then use the higher multiple in the category.

(Source: Get Acquired for Millions: A Roadmap for Technology Service Providers to Maximize Company Value)

* MSSPs will always be at the top of the range in each revenue category.

EBITDA Multiples Vary by Organization Size

The reason we have such a plethora of rollups in the IT space is exactly what is illustrated in this chart. Notice how a VAR under $10M is valued as low as 3x, but as soon as it reaches $25M, it can get valued as high as 9x or more. It is really hard for a company that is under $5M to really get above a 5x multiple, in part because it is so small.

The smaller the company, the larger the risks; meaning a loss of a major customer, employee, or even margin adjustments from a major vendor can make a big impact. Savvy buyers know this is an inherent risk of a smaller company.

But there are things you can do to help mitigate these risks as a smaller company. Start with minimizing customer concentration and expanding your products to selling those that produce higher margins. Shift your focus from billing by the hour to billing packages for services. And always, always work on increasing the recurring revenue. At a minimum it will get you to the highest multiple for your size and organization type.

And that’s the goal, right? Preparing well for a sale, so you can get top dollar for your company.

7. Why MSPs Sell for a Higher Multiple Than VARS

While it’s true that the technology service industry is still a hot bed for mergers and acquisitions, it’s also true that there is a big gap between what a VAR can expect to receive for their company versus an MSP or MSSP.

I know that may come as a surprise to some. And here’s the thing: MSPs/MSSPs almost always receive a higher offer than VARs with the same net income.

Not the greatest news for VARs, I know, but there are valid reasons why, which I cover in my blog: Why MSPs Sell for a Higher Multiple Than VARs

I also cover the circumstances where a VAR can catch up to MSP multiples.

Let me give you an example of the difference in multiples. Let’s compare two IT service providers (a VAR and an MSP), both with basically the same numbers:

- EBITDA value is $800K

- Both have over 40% in recurring revenue

- Both have no one single customer representing more than 10% of total sales

The EBITDA multiples for the VAR might range from 4x to 6x, whereas the EBITDA multiples for the MSP will range from 6x to 8x! That’s a difference, easily, of a 2x multiple (2 x $800K) or $1.6M, if not more.

I have seen this type of variation in my own deals recently. And it’s important for both VARs and MSPs to know WHY buyers are providing different offers between these two seller types.

Having this understanding helps a seller know how to position themselves to buyers, how to have informed conversations with them, and realistically set their own value expectations.

Take a look at the article to learn more.

And VARs, don’t dismay – I had a VAR seller who ended up having to choose between 12 offers! So there is definitely still demand, and you can accomplish a very successful transaction. You can find the link to that story in the article as well.

8. EBITDA & Normalizations – The Hidden Money

If you are a business owner, I’m sure you are familiar with EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). This is considered the traditional valuation method that measures a company’s historical cash flow generation. Usually a multiple of this number (depending on the type of company) is used to value a company – anywhere from 3x to 12x in the technology space, unless of course you have your own IP, then valuations can be north of 15x.

As described above, the calculation of EBITDA is simple, so we won’t dwell on that here anymore. But it’s the normalizations where you find the money!

Why? Because all those hidden add-backs (and some subtracts) can add thousands, if not millions, to your enterprise value.

Let’s look at a couple of “real-life” examples:

Maybe you own the building that you currently occupy, and you not only deduct rent, but all the expenses associated with running a building through your P&L. Even if you have that building in a separate entity (most people do), you still tend to take the expenses of keeping it maintained on your books. In a recent transaction, we found close to 100K in extra building-related expenses on the P&L. With a valuation of 8x EBITDA multiple, this was another $800K to the bottom line.

Or maybe you have been using an outside accounting firm to help keep your books on a GAAP basis because you don’t understand all the nuances, but know you want to enter into a sale transaction. So, although you can run your books on a cash basis without help, you pay for this extra monthly accounting fee. Let’s say you spend $4K a month with an outside firm ($48K per year). That add-back at a 6x multiple is another $288K in your pocket.

Most sellers don’t look for these special add-backs, and therefore leave money on the table. And unless you have a really, really good M&A advisor who understands accounting (most don’t), many normalizations are missed.

Even in my own last transaction, I found items on my own at the very last minute that my broker had no idea to look for. This included margin changes in my favor that would start a month after the sale, and that would add another $50K to my bottom line if retroactively applied. It also included commissions to a related entity that I would no longer be paying.

Normalizations are everywhere if you know what to look for. Below are just a few example, but you can go to my blog post to get a more in-depth list.

Add-backs to your EBITDA number (increases your value):

- Excessive owner salary: Owners earning far above the industry norm.

- Owner Bonuses: Amounts pro rata beyond what other employees are receiving. But don’t include distributions via your S-corp in this number.

- Profit Sharing: Owner profit sharing or 401K beyond a normal 3% match, etc.

- Automobiles/Housing: While completely legal, the buyer would likely not embrace moving forward.

- Insurance (i.e., owner’s health, auto, life, key man, disability): The new owners may not provide all of these or pay for all your family members.

- Owner Travel: If excessive between locations.

- Legal Expenses: Perhaps due to a one-time lawsuit.

- Contributions: Owners many times have their favorite charities, which may be considered a more personal item.

Of course, there are things you will need to subtract as well. Again, be sure to go back to my blog post to read those. And don’t forget about those COVID adjustments as well. Again, an entire paragraph dedicated to that in my post.

Basically, the point here is that there is a lot of money to be found in normalizations. So either enlist a good M&A advisor that knows how to find these, or consider paying for your own Quality of Earnings (QofE) Report to have an outside professional find more. It’s worth the cost either way!

9. Recurring, Repeat and Renewals – Each Have Different Value

If I only understood this concept earlier… Oh boy, I could have sold one of my companies for sooooo much more. But I didn’t, so I left money on the table.

As owners, we just look at “revenue” as one big lump sum number at the end of the year. We don’t focus necessarily on growing one type of revenue, but instead on the total number.

Hopefully, after reading this post, you will start looking at your revenue differently!

Let’s start with this….

If all you do in the next year is focus on growing your recurring revenue – even if you don’t grow top line revenue by even $1 more – you have increased the value of your company!

Yes, reread that again, and let it sink in. That is how dramatically important recurring revenue is to your company valuation.

Want one other big insight? Make sure that the recurring revenue is contractual – meaning that your customer is obligated for at least one year to pay it. You don’t need long, three-year contracts like years ago for that revenue to be considered recurring. Of course, ideally you want your one-year contract to be evergreen, where it renews on its own.

Let me give you a real-life example of how a contractual recurring revenue customer saved one of my clients from losing value in the last week of a transaction:

We were 5 days from close and the buyer wanted to reach out to the top customers as their last step in the due diligence process; a very common practice. While every customer came back with a raving review of my client, one did mention that they were planning on cutting their Microsoft Office seats by a third due to layoffs in their industry (in this case, over 100 seats)! This, of course, caused a great amount of concern for the buyer because this was the seller’s largest client, and they were going to drastically reduce seats. But a closer look at the agreement also showed a plethora of other support services that the client was contractually obligated to pay for over the remaining life of the contract, which happened to be another 9+ months and had nothing to do with seat counts. This accounted for the vast majority of the month’s fees, so reducing seat counts by 100 or so didn’t have a drastically material effect on the monthly bill. Plus, the customer was contractually obligated for another 9 months to pay these monthly fees. With all the other pending opportunities in the seller’s sales pipeline, the buyers decided to close the transaction as was written in the LOI without changing any of the terms. Had this NOT been a contractual agreement, this could have ended much differently.

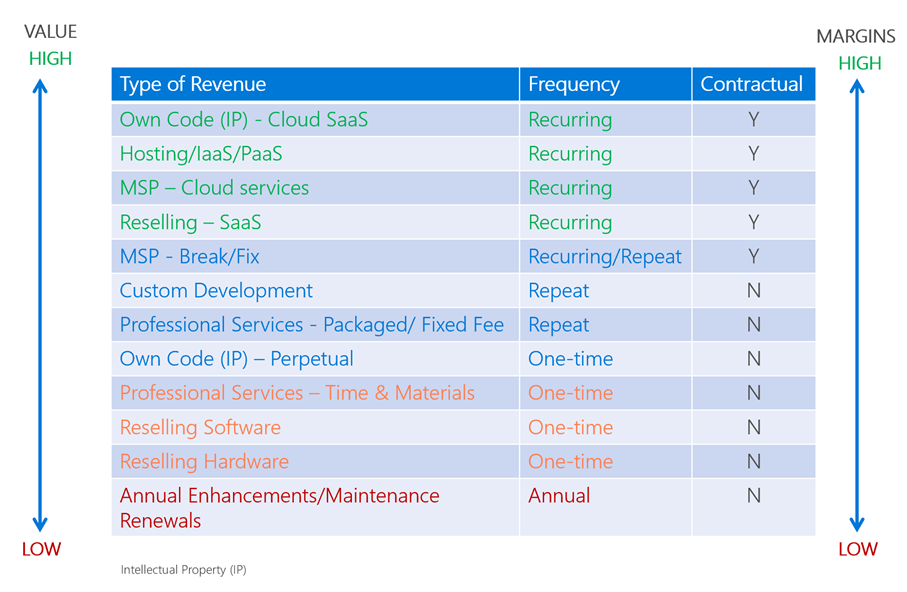

As a refresher, recurring revenue is typically revenue that is contractually bound by a legal agreement for a solution delivered by either a vendor or the partner organization over time.

Repeat revenue, on the other hand, is revenue that typically happens every year, but is not contractually bound on an annual basis. Custom developers are a great example of technology service providers who have a high amount of repeat revenue.

Finally, there is renewal revenue, which unfortunately is the least valuable because there is no value-add by the provider – meaning all you are is the pass-through entity who is selling the maintenance plan and not the person actually supporting it. Many partner organizations like to call this repeat revenue because it does typically happen every year, but unless you can attach some of your own services to it and can show this keeps the customer over many years, it remains renewal revenue.

Why is this all so important? Each TYPE of revenue has its own value.

Here is a handy chart that details the value of revenue by category. The highest value revenue is at the top in green and the lowest is in red at the bottom. For more information on this, read this in-depth post that describes the revenue types in detail.

The point of this post: when you think about your revenue in 2024 and forecast out these amounts by month, also pay attention to the streams of revenue in your business. Be sure to always focus on recurring revenue, ideally contractually bound (those in green), but be thankful for any repeat revenue you can attract as well. If you really want to drive the value of your business through predictable and reliable recurring revenue, think about how you might make it harder for your customers to consider your competition; turn them into lifetime customers instead.

Remember the value is not in how much revenue, but instead what type!!

10. The Number You REALLY Need to Sell Your Business For

When starting to think about selling their company, one of the first questions in most sellers’ minds is, “How much is my company worth?”

And while this is a very important question, there’s another vital question that can be overlooked:

“How much do I NEED to sell my company for to comfortably retire?”

I call this amount your Great Resignation Number.

This number lets you live your ultimate lifestyle after you exit, whether you’re walking off into the sunset or continuing to work post-acquisition. That’s what you’ve been working toward for all these years, right?

To help you easily figure out what this number is for you, I created a NEW and IMPROVED version of my Great Resignation Number worksheet.

This version 2.0 is even more detailed and comprehensive than the original.

In this easy-to-use Excel worksheet, simply follow the instructions and examples to plug in your own numbers, and it will calculate your target asking price.

Considering rolling some equity as part of the sale? We covered that too.

Download the worksheet today and take the ambiguity out of your future goals!

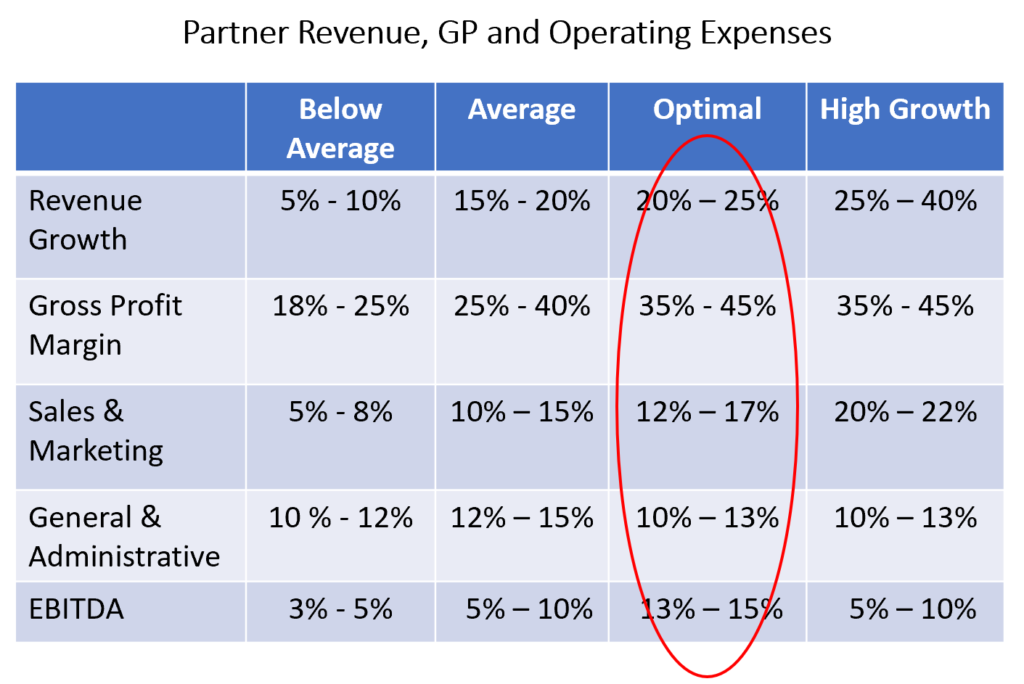

11. Best-in-Class Numbers – What %’s Should You Be Striving For?

This week in our Get Ready to Sell series, I want to share with you what we call best-in-class numbers (percentages), and what you should be striving to hit or exceed when it comes time to sell.

Here are the key sections of your P&L that we will focus on:

- Revenue growth

- Gross Profit Margins

- Sales and Marketing expenses

- General and Administrative expenses (which is everything else)

- And finally, EBITDA percentages

Almost every prospective seller wants to know how their numbers are stacking up against the competition. Remember from earlier emails: I am not a big fan of comparing yourself to your competition, but there ARE numbers that you should be striving for. So, I thought I would share these with you. We have an entire module on this in my course, Ready…Set…Sell, and I also wrote an in-depth blog about them here.

But in short…. You want to strive for the OPTIMAL category, as shown below, each and every year for few reasons:

- They hit the Rule of 40 test*

- They are what the best companies produce

- These are numbers that are achievable over an extended period of time. This is key!

Best in Class Numbers

One might assume that the High Growth category is the ideal category to be in. And it is, if you can maintain that level of growth consistently year over year. But generally speaking, a growth rate of 25% – 40% is hard for most partners to sustain year over year as revenue increases. And it’s really hard to sustain for more than 3 years in a row, which is what most buyers will look for when reviewing your financial data. That is why the Optimal category is more consistently achievable. Again, consistency being a key factor.

One might assume that the High Growth category is the ideal category to be in. And it is, if you can maintain that level of growth consistently year over year. But generally speaking, a growth rate of 25% – 40% is hard for most partners to sustain year over year as revenue increases. And it’s really hard to sustain for more than 3 years in a row, which is what most buyers will look for when reviewing your financial data. That is why the Optimal category is more consistently achievable. Again, consistency being a key factor.

To read more on the topic, see my full blog post here. I go into much more detail.

And yes, the Average column truly is what I see on average, so you want to be sure to beat those numbers!

Next week we shift the focus to how much you might expect to pay for fees in a typical M&A transaction.

I look forward to seeing you back here then.

* If you don’t remember what the Rule of 40 is, I cover it in this article. It is a simple financial framework that has become somewhat ubiquitous as a way to determine how successful a company is.

12. Common Seller Fees in an M&A Transaction

Let’s pretend that that you have an LOI and transaction close date just around the corner. At this point, you can expect a few expenses to come out of the millions that you are selling your company for.

Besides the sale bonuses you are giving your team and potential equity you are investing in the new company, there are a few very common seller fees you will encounter as part of an M&A transaction:

- Advisor Fees (Investment Banker, M&A Advisor, or Business Broker)

- Attorney Fees

- CPA Fees

Other expected fees include:

- Indemnification Escrow

- Tail Insurance

(There are likely other amounts that will be subtracted from the closing amounts, but let’s just focus in on the fees listed above for now.)

Last year, I wrote a pretty extensive blog on the various M&A fees you will encounter in a transaction. But I wanted to update you with a more recent fee schedule according to an M&A Fee Study done by Firmex.

Advisor Success Fee

Most M&A advisors work for a success fee. A success fee can either be a fixed specified number or calculated as a percentage, depending on deal size as follows:

- 4% – 6% for $5M – $10M deals.

- 2% – 4% for $20M – $50M deals.

- 1% – 2% for $100M – $15M deals.

The success fee is payable at closing either as part of the funds distribution or as a separate wire directly from the seller.

You can find more info on other types of advisor fees, specifically attorney fees and CPA fees, in my article: Common Seller Fees in an M&A Transaction

You’ll also find details on two other expected fees (tail insurance and indemnification escrow), as well as an example of what these fees might look like in a real transaction.

13. Common M&A Agreements

We are now at topic 12 of our email series, Get Ready to Sell in 2025 (and beyond). If you missed a few already, don’t worry; we will have a midway recap soon of all the topics we’ve covered in the first half of the series so you can catch up.

Did you know that the typical M&A transaction will have at least 8 – 10 agreements as part of the entire document group called the “Definitive Agreements?” Most first-time buyers/sellers assume there is only one agreement (the Purchase Agreement), which is a huge misconception.

In our last post we reviewed legal fees and how much they might be in a typical M&A transaction as a seller. We can wrap a little more context around those fees because, as you just read, there are multiple agreements that your legal advisor will need to review.

Here are the typical agreements I see in a standard transaction process:

- Broker – Seller Agreement: The Seller Agreement specifies the terms and conditions for how, what, and how much you will pay your M&A Advisor, Investment Banker, or Broker.

- Non-Disclosure Agreement: The agreement where Parties understand that each is willing to share Confidential Information with the other for the purpose of considering a business relationship.

- Indication of Interest or Expression of Interest (IOI or EOI): An IOI is a non-binding letter prepared by the buyer for the seller. The main purpose is to express a genuine interest in purchasing the company before the issuer has had the opportunity to review sufficient data (due diligence).

- Letter of Intent (LOI): The LOI is a document that outlines the terms of an agreement. While this is typically non-binding, it is important to list out the key aspects of the deal in this document as it will serve as the foundation of the definitive purchase agreement.

- Stock or Asset Purchase Agreement (SPA or APA): Purchase agreements are legally binding contracts between shareholders and companies. Also known as share purchase agreements, these contracts establish all of the terms and conditions related to the sale of a company’s assets or stocks.

Find more information on other agreements commonly found in a deal, and how much these agreements tend to cost as a buyer or seller, in our newest blog: Common M&A Agreements.

And If you want to learn more about these documents or get examples of actual documents used in transactions, we have created M&A document templates for both buyers and sellers. Whether you are buying or selling, its good to see samples of what these documents can and will look like so you can be prepared for your own transaction.

14. Normalization Adjustments Are NOT Just Personal Expenses

What is one of the most central factors to increasing the enterprise value of your company? It’s not net income or even your EBITDA, but your normalized or adjusted EBITDA.

Increasing this through normalizations/EBITDA adjustments/add-backs undoubtedly increases the value of your company. Unfortunately, most sellers don’t know this and can leave lots of money on the table.

But, luckily, that’s not going to be you, because I discuss the 8 most common categories of EBITDA adjustments in my article: Normalization Adjustments Are NOT Just Personal Expenses

After having worked on dozens of seller financials, I have devised my own system for uncovering normalizations so that none get missed. And now, I am sharing these with you.

In case you’re new to the topic, normalization adjustments are the adjustments that you will make to your net income (either increase or decrease) that remove all the non-essential, one-time, or personal expenses that you run through the company that won’t happen post-sale.

Notice how I didn’t just say personal expenses? These adjustments go far beyond just that.

So, take a look at my article to make sure you understand what you can add back to increase your value. I clearly lay out the 8 categories of typical adjustments I look for when reviewing my client’s financials, including examples of items that fit in those categories.

Remember, every dollar you find here is multiplied by the multiple you sell for.

So, for example, if you find $300K of adjustments over the last twelve months and the typical multiple for your size company is 6x, then you just added ($300 x 6x = $1,800,000) to your sale price.

Worth the effort, don’t you think?

15. From Planning to Profit: A Comprehensive Guide to Successful M&A Transactions

Hopefully by this point in our Get Ready to Sell email series, you’ve learned that the most successful M&A transactions happen to those who plan and prepare in advance.

But with so much information and advice out there, it can sometimes be difficult to know exactly HOW you should plan and prepare.

Detail and nuance is important to understand, as every company is unique. But there are general steps that almost every company should take to begin working toward an eventual successful sale.

That is exactly what I provide in this article through 10 straightforward steps (with plenty of helpful links): From Planning to Profit: A Comprehensive Guide to Successful M&A Transactions

As I’ve mentioned: for most companies, it’s a good rule of thumb to start preparing at least 3 years in advance of your expected sale date.

And this checklist includes everything from management, to financials, to due diligence, and everything in between.

It’s the perfect place to start if you’ve been following along with this email series but just don’t know where to begin.

And trust me, you want to have a game plan before you get into the weeds of the most important deal of your life.

Let this guide serve as an easy step one toward your smoothest, most valuable future transaction.